The Mutual Home Ownership Society Housing Model

The Mutual Home Ownership Society (MHOS), formed by LILAC Cohousing in the UK in 2013, is an innovative housing model through which Killick Ecovillage Co-operative is transforming both market and non-market housing.

How? MHOS empowers future residents of varying income levels and does not involve individual homeownership like in the traditional housing market. Residents of the Killick Ecovillage Co-operative collectively own the community’s homes and buildings and are dedicated to maintaining, funding, and operating them efficiently.

What is market and non-market housing?

Market housing is traditional private housing in which individuals are the only owners of the homes. Non-market housing is owned and operated by a government agency or a not‐for‐profit society.

When you become a Killick Ecovillage resident, you act as a lender rather than an owner or a renter. The Co-op takes a loan from you up to the value of your home, which is repaid over time with interest if you leave the community. That is how we all become co-owners of the ecovillage. And the small return you do get for your loan is not market-tied.

Because we are a co-operative, members never have more ownership than others. Regardless of their income level, all residents have an equal say and investment in their future high-quality neighbourhood.

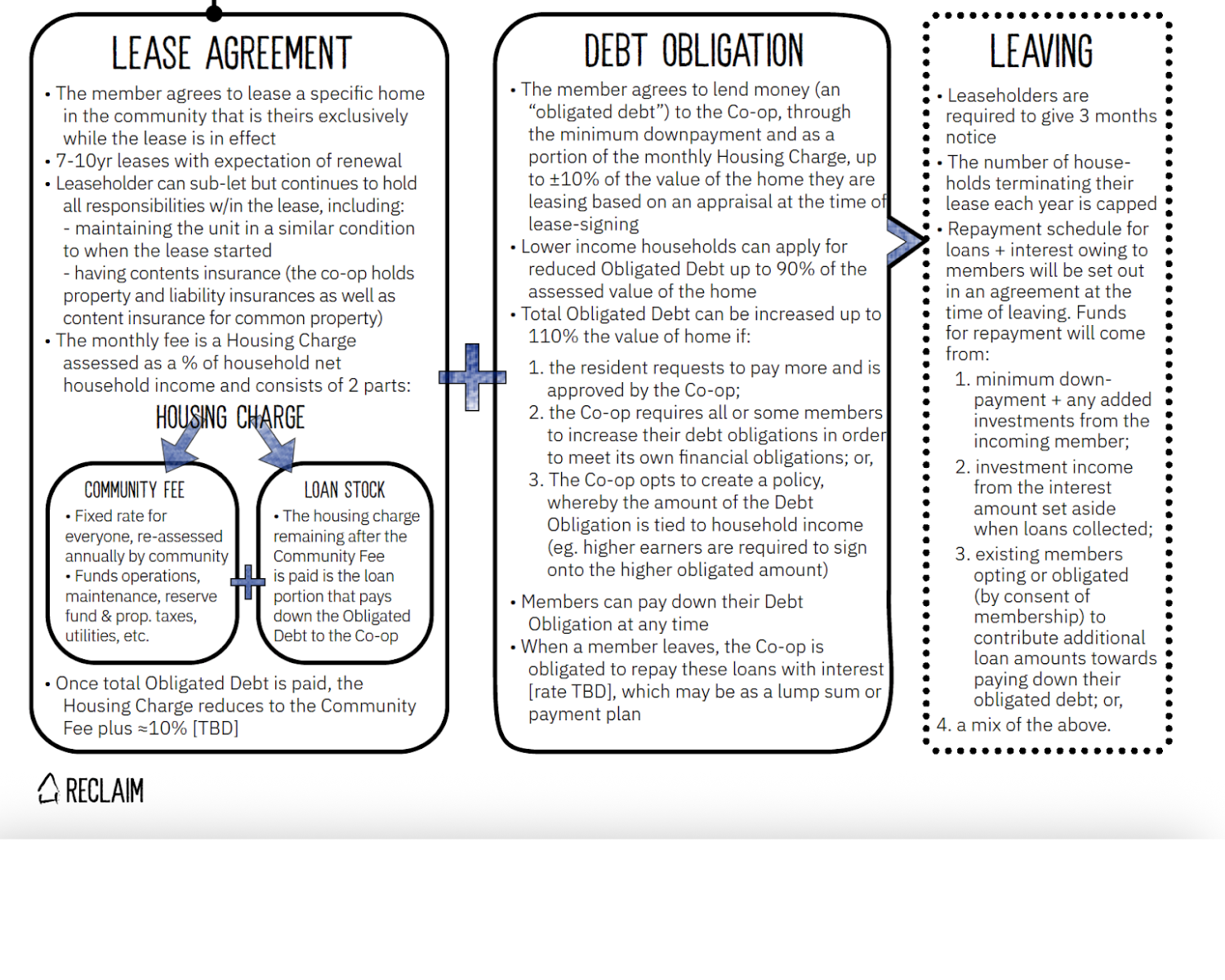

The loan you provide is a set amount called Total Obligated Debt, which is lent over time via:

- A Minimum Initial Loan (about $15k), which is the initial amount of money lent by the member to the co-op. It is the equivalent of a “down payment” in the traditional private housing market. If you don’t have the full amount, you can enter into a payment plan.

- Regular contributions are built into the monthly housing charge.

- Additional voluntary contributions.

Housing Charges through the MHOS Model

The payments above are included in the overall monthly fee each member is charged, based on a percentage of their household’s net income—currently modelled at 30% —to ensure affordability over time. This fee is broken down into three components:

1. Community Fee:

Set annually, through member participation, to equally distribute the co-op’s operating expenses across all member households. This fee covers property taxes, insurance for the common areas, utilities, repairs and maintenance, garbage and recycling management, staff fees, and Replacement Reserve inputs. Killick has included a $100/month food program in this fee to cover on-site food production, shared meals, and bulk purchases. When the income-assessed housing charge is lower than the Community Fee (typical for households earning below 30% Area Median Income-AMI), the difference is a subsidy paid through the Community Fund.

2. Loan Contribution:

Anything above the Community fee up to the Median Market Rent (MMR) rate for the home the member occupies is contributed as a loan to the co-op that is transferred into the Community Fund. The combined Loan Contribution and Community Fee is the member’s “basic rent”.

3. Voluntary Loan Contribution:

This is the difference between the basic rental amount and the income-assessed housing charge. This voluntary loan goes into the Community Fund and helps a member pay down their Total Obligated Debt faster while also supporting the Community Fund program.

The Community Fund is the “single pot” that combines all of the loans from Killick resident members, ensuring ongoing affordability and financial sustainability for everyone. The Community Fund is used to cover operating budget deficits, generate passive income through investments, and provide funds to the co-op to repay members when they leave.

The income-assessed structure enables you to pay the fee based on your income. Lower earners are effectively involved because higher earners will pay faster and subsidize them in the short term. Over time, however, everyone contributes their fair share—a win-win!

This graph illustrates the MHOS process for Resident members: Entering into a lease agreement for 7 to 10 years once you choose a house (expectations as a lessee, the monthly fee over time), the debt obligation (lending conditions, options for lower earners, repaying the loan), and what happens if you leave the ecovillage (conditions to be able to leave, repayment schedule, and sources of the funds to be repaid).

Still have questions? Please contact us.